The good news is that the Federal Government is ensuring that more people aged 67 and above can access the Age Pension.

But the confusion and complexity around means testing has to be confronted before more money flows your way.

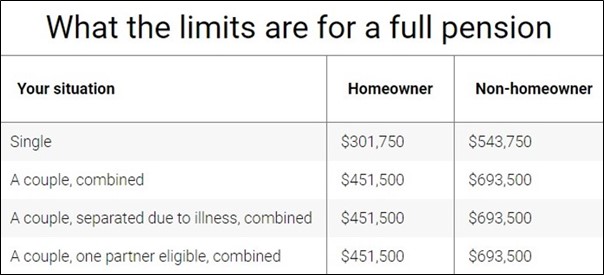

The Age Pension increased on September 20, as did the assets test limits above which no Pension is paid.

The asset test limit for a single homeowner rose $11,000 to $667,500 of assessable assets and for couples, it increased to $1.003 million, up $16,500.

Non-homeowners get higher thresholds still, and the rules around assets, income tests, taper rates and deeming rates open avenues to a number of financial strategies that will deliver seniors more Pension.

Who gets an Age Pension?

Almost 2.6 million Australians currently receive a full or part Age Pension, with another 773,000 on a disability support pension.

The Centrelink Financial Information Service provides free advice, education, and calculations, but it is also recommended that people seek professional financial advice.

“If you do a half a million dollars of renovations on your property to access $5,000 in Age Pension, you could be generating $25,000 of income having it sitting in a bank account, or $40,000 of income if having it sitting in a good share portfolio,” said Pivot Wealth Founder and adviser Ben Nash.

“It doesn’t add up from a numbers perspective.”

Homeowners better off under Pension asset tests

Ben says the best situation is to retire in your home and be debt-free.

Homeowners have a much better deal than non-homeowners when it comes to accessing Pension payments.

Non-homeowners get higher asset test thresholds; however, the difference is only $242,000 – well below the cost of a home.

Depending on where you live, there can be Council and water rate discounts, cheap or free transport, energy bill discounts, lower motor vehicle registration costs, cheaper medicines, and bulk-billed doctor visits.

Superannuation

Money held in superannuation is exempt from Centrelink asset and income testing until the fund member reaches the Pension age of 67.

This does allow financial maneuvering where a pensioner’s partner is younger.

Hundreds of thousands of dollars can be transferred to the younger spouse’s super, effectively hiding it until they reach Pension age. Planning may need to start early for this because of gifting and superannuation rules.

Death of a partner

When one partner passes away, there’s a reasonable chance that the survivor’s changing status from a couple to a single for assets test purposes stops them having a Pension.

Good financial planning and estate planning can help preserve Pension payments by directing some assets to children and grandchildren through wills or superannuation, and the use of other financial products such as annuities and investment bonds.

Find out more HERE.

Note: This article offers general advice and is not a substitute for personalized financial guidance. Consult a financial professional for advice tailored to your specific circumstances and needs. The author and publisher are not responsible for individual financial decisions made based on this information.